Goals

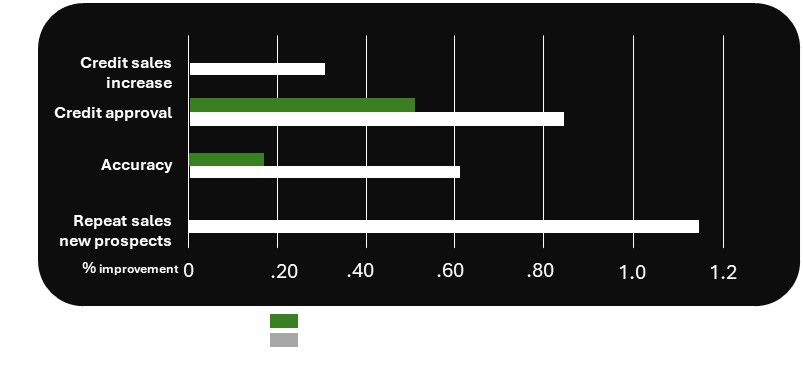

The goals of the retail store's instant customer credit approval program were to increase sales among new prospects by more than 5%, deliver credit decisions at the point of sale in under two minutes, and achieve a success rate exceeding 85% for repeat business driven by ML-approved credit decisions.

Business Value Achieved

Project Results

Project Overview

AI and machine learning were used to enable instant credit card approvals by analyzing multiple backend data sources, including credit reports, mobile phone data, and other demographic information. The system generated dynamic, personalized questions for new customer prospects, and their responses were evaluated in real time to determine approval or denial ("thumbs-up" or "thumbs-down") for in-store credit. Results were displayed directly on existing IBM point-of-sale terminals, eliminating the need for costly store retooling or additional checkout hardware.

The Problem

A large retail organization faced a costly mainframe upgrade to implement a new instant credit solution aimed at supporting impulse purchases among younger customers with limited credit history. The planned approach relied on hard-coded business rules and required developing new applications to replace the existing point-of-sale (PoS) systems.

The Approach

An open-source solution was introduced that replaced hard-coded rules with AI/ML-driven decisioning, enabling dynamic searches across demographic and publicly available data sources. The system generated up to seven targeted questions for new customer prospects, and their responses were evaluated against backend machine learning models to determine instant credit approval or denial ("thumbs-up" or "decline").

Because the solution was lightweight, the existing point-of-sale (PoS) system required only minimal modifications to call the ML service and display results directly on current equipment. This approach eliminated the need for costly infrastructure upgrades and a full application re-build.

Retail Sale Improvements

Project Insights

During the project, several key insights emerged:

- Machine learning performance improved when validated against third-party backend credit scoring results.

- For young women with no formal work history, non-traditional indicators — such as volunteer work and related activities — proved effective in assessing creditworthiness.

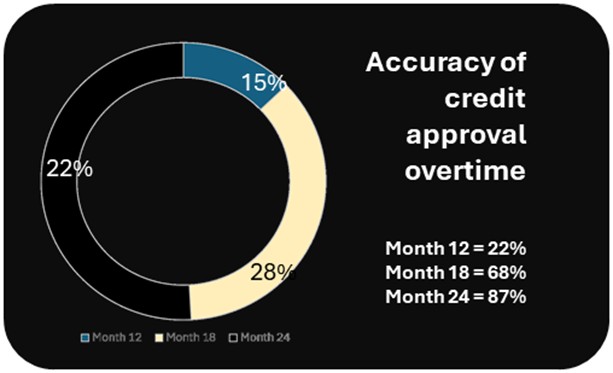

- Early ML outputs required human intervention to retrain models and refine dynamic risk questions, leading to improved accuracy over time.

- Training and optimizing the ML models took longer than expected, requiring over a year to develop a reliable risk and loss learning curve and achieve consistent approval accuracy.

Summary of Findings

The on-the-spot ML-based credit approval process proved effective in serving young women without established credit histories. It increased repeat sales within this demographic without raising the risk of credit defaults. Additionally, the ML system continuously adapted to evolving patterns, generating new, tailored qualification questions for each prospect as it learned from both successful and unsuccessful credit outcomes.